By

DANIEL

GOLDSTEIN

PERSONAL FINANCE REPORTER

The Federal Reserve’s anticipated rise in interest rates is expected to impact all sorts of real-estate transactions, whether you’re buying, selling or renting. Here’s what you need to know for the coming year if you’re ready to take the big plunge as a homeowner, or finally get that deluxe apartment in the sky.

Home prices may stagnate

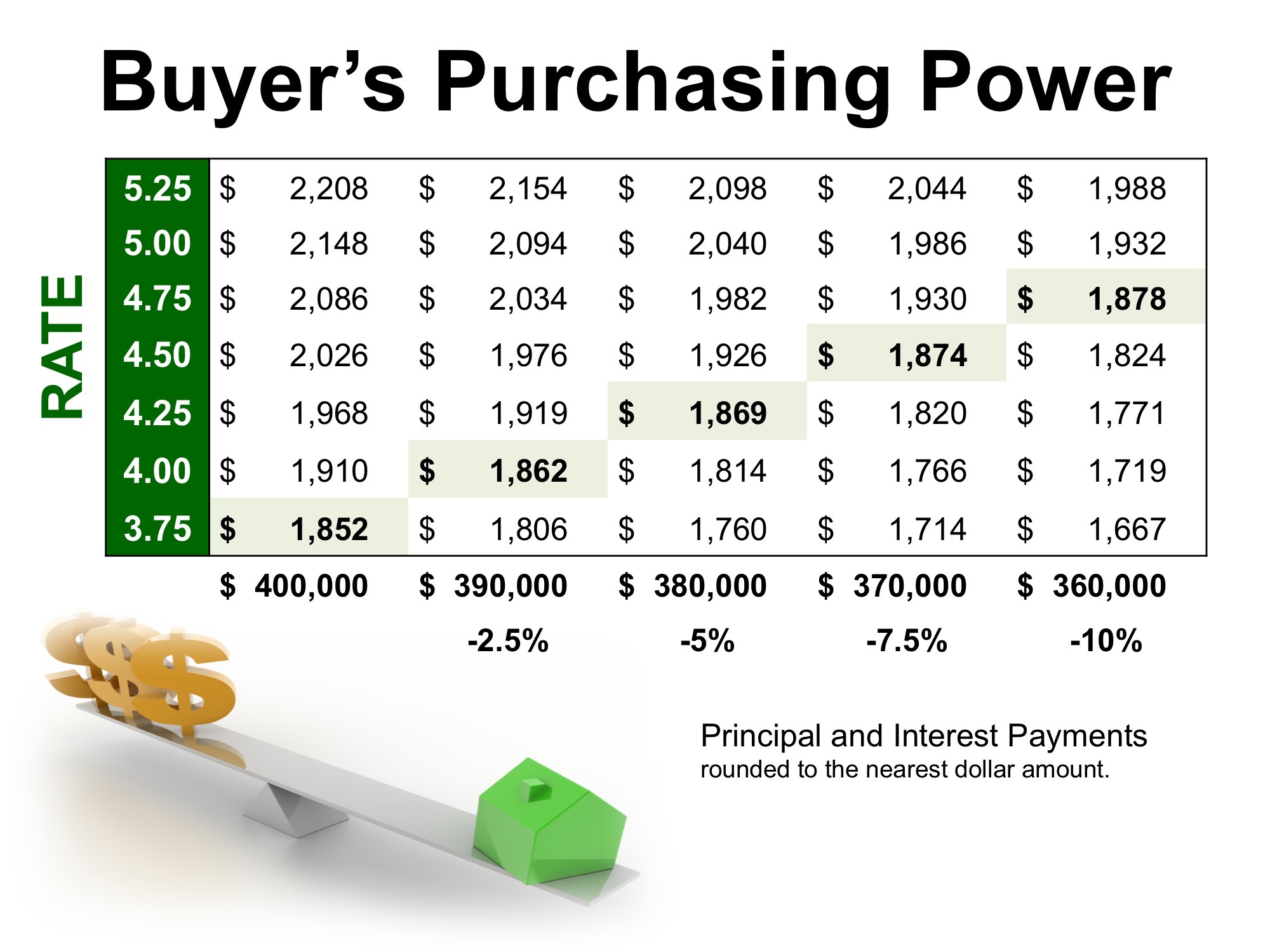

As the Federal Reserve worries less about stimulus and more about keeping inflation in check with an economy that’s finally producing jobs, interest rates will go up, increasing the cost of credit for those seeking to purchase a home.

“Affordability is going to be a much bigger hindrance going into 2016,” said Daren Blomquist, vice president of research at Irvine, Calif.-based RealtyTrac, a realty research group. Blomquist said that currently about 3% of the nearly 600 U.S. counties his firm tracks have home prices that are “unaffordable” to the average American weekly wage earner (who made $1,056 a week in the first quarter of 2015). If interest rates top 5%, Blomquist expects a surge of unaffordable markets.

“If interest rates rise, and home prices rise, and wages rise only tepidly, we could see the 3% of unaffordable markets rise to as much as 25%. Stagnation of home price appreciation would be a likely scenario,” Blomquist said.

Realtor.com (which is owned by MarketWatch’s parent company, News Corp. NWS, +1.39% ) predicts that 30-year mortgage rates will increase to 4.65% on average by the end of 2016, compared with current 30-year rates as compiled by Bankrate.com of 3.88%.

At a 4.65% interest rate with a 30-year term and a 20% down payment of $36,600, a home at the current (November 2015) median value of $183,000 would have an estimated mortgage payment of $945, including property taxes and insurance. That compares to a current mortgage payment of about $879 a month including taxes and insurance at 3.88%

On average, housing prices will rise by 3% nationally in 2016, compared with 6% in 2015, Realtor.com said.

“Healthy economic indicators will be tempered by lack of access to credit and rising home prices, which will ultimately limit housing demand and growth,”Realtor.com economist Jonathan Smoke said in an analysis issued Dec. 2.

Still, in some markets like San Francisco, where the median rent in October hit a record $5,000 a month for a two-bedroom apartment, rather than renting a similar-sized property, becomes a better option. “When rents go up, it actually makes buying more attractive,” said Ralph McLaughlin, an economist with San Francisco-based real-estate research group Trulia.com. “The flip side is that if rents continue to climb, it’s going to make it more difficult to save for a down payment,” he said.

More millennials will look to buy a home

The good news is that more millennials want to buy homes between now and 2018, according to Trulia.com. Just 65% of millennial-aged borrowers (ages 18 to 34) wanted to own a home in 2011, according to the real estate group, but now that number has increased to 80% for 2015, up from 78% in 2014. And one-third of those will want to buy in the next two years, Trulia says. “Most borrowers of this age group are waiting for a work promotion or to build up enough savings to buy,” said McLaughlin. “We don’t expect a big rush to jump in, but it’s going to be an incremental improvement,” he said.

But the Federal Reserve raising interest rates might make some millennials want to hibernate in Mom and Dad’s basement another year. That’s because it increases the cost of credit while many of them are already struggling with crushing student debt loan levels, stagnant job wages, and rising home prices and rents.

McLaughlin said that the federal government’s effort to boost home ownership during the housing downturn was disorganized and scattershot, but it might have found a winner with the reduction in mortgage insurance premiums for FHA loans by an average of $900 a year. “We saw a small but noticeable increase in FHA borrowers after mortgage insurance premiums were reduced,” he said.

McLaughlin sees a further move in 2016 by FHA to lower premiums, but also says the job market prospects for the millennial age group is still being hurt by the baby boom generation that is only slowly retiring and aren’t selling their home. “Baby boomers are working later in life and it keeps a cap on the younger generation,” said McLaughlin. “How can they move up, if they are staying in place?”

There may be fewer houses available for buyers

The steady recovery in real-estate prices in many markets over the last four years (the median sales price of all-sized U.S. homes has risen from $153,000 in January 2012 to $183,000 in November of 2015, a gain of nearly 20%) has been a two-edged sword for people looking to buy a home or move up to a larger or better one.

For one, it’s hurt entry-level borrowers trying to get starter homes. But the flip side is that if you own a home, you’re more likely to take the equity gains and plow them back into improving your home, rather than moving to a larger one, says Kermit Baker, an economist with the American Institute of Architects. “It’s the mortgage lock-in effect,” says Baker.

“People aren’t going to trade in their historically low mortgage rate at this point for a higher one,” he said. Instead, he says that baby boomers are more likely to invest $75,000 in a bathroom or $150,000 in a kitchen than use the equity to purchase a larger home and get saddled with a higher-rate mortgage.

Baker says that’s why the AIA is predicting that home improvement projects in 2016 will likely reach a new high, exceeding the record $325 billion set this year. It could also top $350 billion by 2017, the AIA predicts. There will also be more remodeling of high-end rental properties as interest rates drift higher and make renting more attractive for some. “The remodeling demand in the high-end rental market is really strong,” Baker said.

Another reason there are fewer homes out there for buyers is that many homes are still underwater. “Prices have gone up so much that trading up to the next home will cost an arm and leg, so it’s a disincentive,” said Ralph McLaughlin of Trulia. About 7.9 million borrowers (15% of all mortgaged homeowners) are still underwater, meaning they owe more than what their house is worth, compared with nearly 16 million (31% of all mortgaged borrowers) during the worst part of the real estate crash in 2012, according to Zillow. Z, -0.57%

More new mortgage loan products will be needed

As mortgage interest rates rise, the need for more loan products that don’t require large down payments or years of mortgage insurance premiums is going to rise in 2016 as well, says Anthony Hsieh, chief executive of loanDepot.com, the second-largest nonbank lender in the U.S. “We have a real lack of programs out there for consumers to extract equity,” he said.

The growth in credit, Hsieh said, has been occurring on the nonmortgage side of the table for consumers, who have been able to leverage their improved credit into new cars or boats or personal loans, but not mortgage loans. “You’re looking at consumers who are using their credit availability outside of their homes,” he said. While that works for now, it’s a far more expensive line of credit than what they could unlock with their equity built into their homes, Hsieh said.

Still, the Mortgage Bankers Association is predicting that new mortgage originations for 2016 will rise to $905 billion, up from $821 billion in 2015.

RealtyTrac’s Blomquist said that in 2016 he expects to see more loan products such as Fannie Mae’s loan that allows for multigenerational families to spread the cost of homeownership by counting income of boarders or renters and other family members whose income is counted even though they are not on the loan itself. Blomquist said this type of program should be expanded to “crowdfunding” for multiple families who might want to share on a loan or a home.

Blomquist points to Fannie Mae FNMA, +0.75% and Freddie Mac FMCC, +1.06% beginning to purchase loans with only 3% down payments, or 97% loan-to-value products as a sign regulators are less worried about risk and want to expand credit instead. Only about 11% of the mortgage market has products with down payments of 3% or less, according to RealtyTrac.

Earlier this year, Freddie Mac CEO Donald Layton told mortgage bankers that more low down payment products were needed to “fill in some nooks and crannies left in the mortgage market” that left some borrowers, especially those who were self-employed, unable to get home loans.

“We’ve definitely reached the tipping point where the stakeholders in the markets are less worried about risk,” Blomquist said. “The driving force is growing the market, rather than containing the risk.”

Source :DANIEL GOLDSTEIN; Marketwatch.com